{kind=link}

When mortgage charges fell to round 6% in August, householders jumped on the alternative to refinance.

Within the months of September and October, greater than 300,000 debtors closed on a refinance, together with almost 150,000 price and time period refinances, per the most recent Mortgage Monitor report from ICE.

This pushed refinance volumes to their highest ranges in additional than two-and-a-half years.

And greater than 1 / 4 of October mortgage lending consisted of refinances in a market lengthy dominated by residence buy loans.

Maybe most attention-grabbing, debtors who refinanced in these months noticed a few of the greatest price enhancements in a long time.

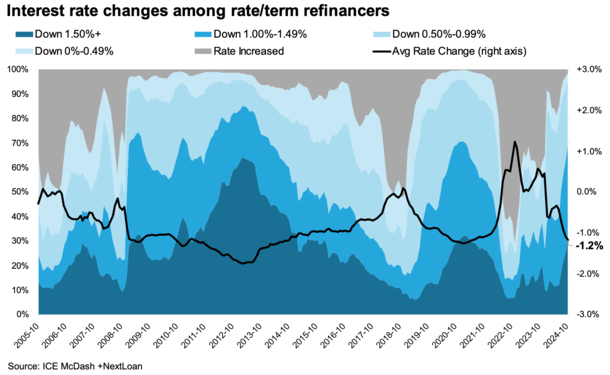

The Common Refinancer Obtained a Mortgage Charge About 120 Foundation Factors Decrease

You’ve most likely heard the phrase marry the house, date the rate. However when you haven’t, it was principally an argument to purchase a house when you needed one, and hope to refinance sooner somewhat than later to get a greater price.

In different phrases, the house is a keeper, however the mortgage is disposable. This didn’t work out nicely in early 2022 as mortgage rates almost tripled from 3% to eight% by late 2023, however it labored out lately.

Per ICE, the common home-owner who utilized for a rate and term refinance diminished their mortgage price by greater than a full proportion level in each September (-1.07%) and October (-1.17%).

This resulted in month-to-month financial savings of $310 and $320 respectively, which is a fairly compelling motive to refinance.

On the identical time, almost a 3rd of those debtors had been capable of cut back their mortgage price by 1.5% or extra, marking the most effective interval for price and time period refis in a long time.

As you may see within the chart above, the darkest blue shaded portion (that signifies a price enchancment of 1.5%+) jumped in current months.

And the lighter shade of blue (1-1.49%) additionally skyrocketed, which means it was a fairly good time to hunt out a decrease mortgage price.

The explanation why was as a result of the 30-year mounted appeared to peak at round 8% in October 2023, after which fell almost two proportion factors in lower than a 12 months.

That large unfold resulted in “a few of the largest price enhancements we’ve seen over the previous 20 years,” in accordance with ICE.

Actually, this mini refi increase has solely actually been rivaled by the 2020-2021 refi increase and the low-rate setting seen in 2012/2013.

So regardless of being short-lived, it was fairly impactful for the debtors who took half.

Most Refinancers Had Solely Held Their Lengthy for About 15 Months

Do you ever take into consideration how long you’ll actually hold onto your mortgage?

It’s an necessary query to ask your self as a result of it could decide whether or not it makes sense to pay mortgage points and/or which home loan type to choose.

In any case, why go along with a 30-year mounted when you count on to promote or refinance just a few brief years later? Why not select an adjustable-rate mortgage comparable to a 5/6 ARM or 7/6 ARM?

Positive, there’s threat concerned if the speed isn’t mounted, and the reductions aren’t at all times nice, however it’s an necessary consideration to make as an alternative of merely going with the default possibility.

Anyway, it seems the common price and time period refinancer solely held their authentic mortgage for 15 months previous to refinancing.

This was the shortest tenure within the almost 20 years that ICE has been monitoring the metric, which tells you people lastly nailed the date the speed technique.

New Know-how Alerts Lenders to Attain Out to Debtors

Whereas it appeared debtors had been on prime of it, you may have the ability to thank new know-how for that too.

Mortgage corporations have gotten so much higher at reaching out to potential prospects when mortgage charges drop.

There are automated methods that can comb a mortgage originator’s database day by day and if charges hit a sure level, they’ll ship out correspondence to potential prospects.

This may clarify why regardless of mortgage charges rebounding larger by late-September, such numerous debtors had been nonetheless capable of snag large financial savings.

Talking of, roughly $47 million in month-to-month cost financial savings had been locked in by householders in simply September and October alone, earlier than rates bounced after the Fed rate cut.

I count on one other refi increase to materialize quickly if mortgage charges proceed on their present downward path.

And chances are high each debtors and originators will likely be able to pounce as soon as once more.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on Twitter for decent takes.