{kind=link}

Preparing article title...

[ad_1]

Every thing has been developing roses for mortgage charges in 2026, however that would quickly change if the Greenland state of affairs spirals uncontrolled.

For the time being, 30-year mounted mortgage charges are hovering round 6%, which is mainly a three-year low.

That led to a surge in house mortgage purposes final week, with each present householders trying to refi and potential house consumers leaping in.

Paradoxically, President Trump’s newest proposal to purchase $200 billion in mortgage-backed securities (MBS) obtained us there.

However his newest risk to impose new tariffs on quite a few European international locations might ship mortgage charges greater once more.

New 10% Tariffs Threatened If Greenland Can’t Be Bought by the U.S.

You’ve doubtless heard of the threats to take Greenland from Denmark, with Trump floating a brand new spherical of tariffs in the event that they don’t conform to a sale.

In a Reality Social publish, he said, “Beginning on February 1st, 2026, all the above talked about Nations (Denmark, Norway, Sweden, France, Germany, The UK, The Netherlands, and Finland), can be charged a ten% Tariff on any and all items despatched to the USA of America.”

“On June 1st, 2026, the Tariff can be elevated to 25%.”

That is in reference to the aforementioned international locations visiting Greenland “for functions unknown” and impeding a sale to the USA.

Trump has argued that the acquisition of Greenland is crucial for “Security, Safety, and Survival of our Planet.”

And that international locations like “China and Russia need Greenland, and there may be not a factor that Denmark can do about it.”

Lengthy story brief, Trump needs to purchase Greenland and if Denmark and its obvious European allies stand in the best way, a brand new spherical of tariffs can be unleashed.

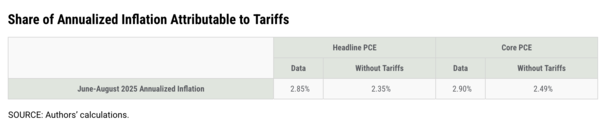

Whereas we are able to argue whether or not or not tariffs trigger inflation till the cows come house, the St. Louis Fed laid out a reasonably good case.

Per the St. Louis Fed, “Over the June-August 2025 interval, tariffs clarify roughly 0.5 share factors of headline PCE annualized inflation and round 0.4 share factors of core PCE annualized inflation.”

To not point out Fed chair Powell stated final summer season that they weren’t able to cut rates as freely as possible due to the unknown impacts of the tariffs.

So whether or not you consider tariffs trigger inflation or not, there’s an honest argument they preserve rates of interest greater than they could in any other case be (CPI vs. mortgage rates).

Mortgage Charges Don’t Exist in a Vacuum

A couple of 12 months in the past, we noticed mortgage charges go on a rollercoaster journey because of the on-again, off-again tariffs.

However they have been arguably caught at greater ranges due to tariffs or the specter of new tariffs.

We noticed the 30-year mounted climb above 7% on a number of events final 12 months, main to a different dismal 12 months for house gross sales.

As soon as numerous that discuss started to wane, and inflation knowledge continued to chill, mortgage rates began moving lower.

In the present day, they’re about one full share level under these year-ago ranges, however that’s partly attributable to worsening labor (jobs reports) and maybe a lot of Trump’s insurance policies now baked in.

And as talked about, the newest proposal for Fannie and Freddie to buy billions in MBS to decrease mortgage fee spreads.

Nevertheless, mortgage charges don’t exist in a vacuum and the MBS deal may very well be utterly overshadowed by this new tariff risk.

Because the St. Louis Fed famous, tariffs accounted “for a significant share of latest inflation.”

The specter of new tariffs (and bigger ones) means inflation estimates might get murky and the Fed would possibly pull again on further fee cuts.

Within the meantime, 10-year bond yields might transfer greater on the uncertainty, pushing the 30-year mounted greater within the course of.

The helpful results of the MBS shopping for may very well be utterly absorbed and we might see mortgage charges climbing again into the 6s as a substitute of falling deeper into the 5s.

As I’ve stated many instances, this is able to be one more gut-punch for potential house consumers (and sellers) and the housing market at giant.

So hopefully we get some readability on this example ASAP to keep away from ruining one more spring housing market.

(picture: David Stanley)

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) house consumers higher navigate the house mortgage course of. Observe me on X for warm takes.

[ad_2]

Source link