{kind=link}

Mortgage charges took one other leg up right now, rising ever nearer to six.50%.

The perpetrator as soon as once more has been the battle within the Center East, which has despatched oil costs surging greater.

That results in inflation, whether or not it’s greater gasoline costs or greater enter prices on items and transporting mentioned items.

Bonds don’t like inflation, so mortgage-backed securities (MBS) costs fall and their yield (aka rate of interest) rises.

That’s what we’ve been seeing because the starting of March and it would worsen earlier than it will get higher.

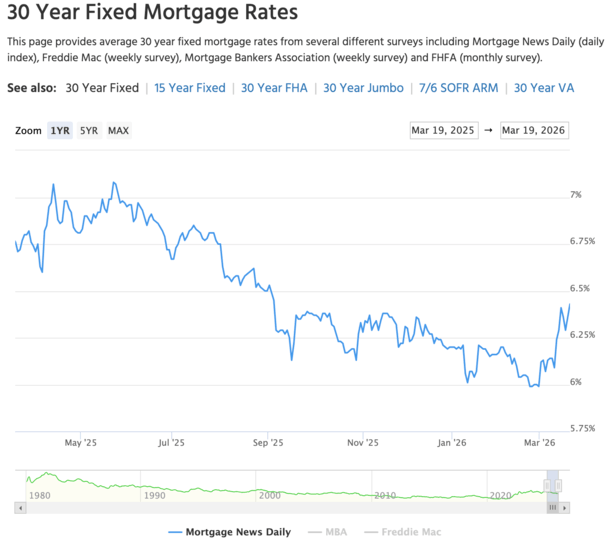

The 30-Yr Mounted Is Again on the Cusp of 6.50%

The newest every day studying from Mortgage News Daily places the favored 30-year fastened at 6.43%, up from 6.36% yesterday.

That’s the best level of 2026, with the earlier excessive being 6.41% on Friday March thirteenth.

It additionally tells you (or a minimum of me!), {that a} 6.50% 30-year fastened is solely a matter of time.

Not a matter of if, however when. We’re banging on the door and the pattern actually feels greater earlier than decrease.

As I mentioned per week or so in the past, mortgage rates stop trending lower and began trending higher, one thing that hasn’t occurred for a really very long time.

Had there not been this battle in Iran, mortgage charges would probably be properly under 6% right now.

As a substitute, we’re going through the worst charges since practically August, which is horrible information for potential dwelling consumers and people searching for a rate and term refinance.

Given there’s no signal of a decision anytime quickly, I’d guess on mortgage charges shifting greater earlier than they transfer decrease.

How excessive is one other query, however ideally they don’t go a lot greater as that is maybe a “transitory” problem.

Each oil costs and mortgage charges jumped up unexpectedly on the Iranian information, however may quiet down for a similar causes because it’s one particular problem versus a widespread financial narrative shift.

Might Mortgage Charges Attain the 7% Vary Once more?

Is a return to 7% mortgage charges attainable?

What as soon as felt unthinkable is now again on the desk because of geopolitics.

I don’t assume we go fairly that prime, although I do assume mortgage charges preserve shifting greater within the short- and medium-term.

In different phrases, I positively assume we blow previous 6.50% any day or week now, a minimum of by MND’s measure.

And likelihood is we go even greater than that because the months go on.

That might imply a 30-year fastened at 6.625%, 6.75%, and even 6.875%, however I don’t foresee a 7% 30-year fastened once more.

Positive, something is feasible, however I feel plenty of what has transpired is already mostly baked into 10-year bond yields.

They have been sub-4% in late February and nearer to 4.30% right now. That’s a giant bounce in a brief period of time that displays what’s at the moment occurring.

Bond yields may re-test 4.50% ranges as this drags on and if mortgage spreads are round 200 foundation factors (2.00%) or barely greater, you’ll be able to foresee a 6.75% fee.

However attending to 7% looks like a stretch.

If we did get again to a 7% mortgage fee and it made the headlines, I feel it could be an excessive amount of for the housing market to bear.

Finest-case situation proper now’s charges quiet down quickly and don’t transfer a lot greater.

It gained’t be nice for the spring dwelling shopping for season, however staying under year-ago ranges can nonetheless be seen as a win.

Earlier than creating this web site, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) dwelling consumers higher navigate the house mortgage course of. Comply with me on X for warm takes.