{kind=link}

Preparing article title...

[ad_1]

Mortgage Q&A sequence: “What’s a letter of rationalization for a mortgage?”

Should you’re at present going via the joyful technique of acquiring a house mortgage, you could have been requested to furnish a “letter of rationalization,” in any other case generally known as a LOE.

Merely put, it permits you to present a bit extra coloration to what the underwriter would possibly really feel is a sophisticated matter.

You may consider the mortgage underwriter as a house mortgage sleuth, one employed to uncover something irregular which will present up in your mortgage file as documentation is submitted.

Positive, the required paperwork would possibly all be there, and your credit score rating and DTI ratio is perhaps spot on, however it’s the underwriter’s job to learn between the strains.

In any other case, mortgage purposes actually could possibly be fed via automated underwriting programs and that may be the top of it. We wouldn’t want human beings anymore.

This isn’t the case, at the very least not but, so count on your mortgage software to be scrutinized, and be ready to “clarify your self” if something that the underwriter feels wants explaining comes up.

Undoubtedly don’t argue with the underwriter or be defiant, that’s by no means an excellent technique. After I labored for a lender, I all the time went out of my technique to be good to the underwriters. You need to too.

Finally, the faster you may get them the solutions they want, the quicker you may get your property mortgage closed and transfer on along with your life.

What Is the Objective of a Letter of Rationalization? It Relies upon

- You lately modified jobs

- You have got uncommon deposit exercise in your checking account

- Latest giant deposits

- Hole in employment

- You have got declining earnings

- Your supply of earnings wants rationalization (self-employed debtors)

- Undisclosed funds (liabilities) out of your checking account

- You have got scholar loans

- New accounts in your credit score report (newly opened bank cards)

- Credit score inquiries in your credit score report

- Different addresses in your credit score report

- Different names in your credit score report

- Notes in your credit score report that want rationalization

- Former delinquencies that want assessment

- Occupancy issues (is it actually your main residence?)

If you apply for a mortgage, you’ll both be accepted or denied. If you’re given the inexperienced gentle, the approval will really be a conditional loan approval.

This implies you continue to have work to do to get to the funding desk. It will entail submitting each prior-to-doc (PTD) circumstances and prior-to-funding (PTF) circumstances for last approval.

A type of PTD circumstances is perhaps a letter of rationalization to clarify one thing the underwriter wants extra readability on, akin to a latest job change or an unusually giant deposit.

It’s so simple as that. The LOE is written and submitted by the borrower with a purpose to present clarification.

Letter of Rationalization Necessities Will Range by Lender

There are many conditions the place a letter of rationalization is perhaps required, too many to call actually. And possibly new ones being generated day by day. However I listed a bunch above.

Moreover, the necessity for an LOE will fluctuate by mortgage lender. Not all of them would require one relying on the state of affairs at hand.

Finally, some lenders and underwriters might be extra stringent and/or cautious than others.

That being stated, a number of the extra widespread ones are likely to do with belongings aka cash, and the place it got here from.

For instance, when you supplied financial institution statements to fulfill one in all your mortgage circumstances, the underwriter would possibly flag a number of the transactions or deposits upon assessment.

Maybe there’s a deposit for $10,000 within the account, which doesn’t fairly line-up with what you make in the best way of wage. It appears a bit misplaced, even when it’s fully legit.

The underwriter could ask that you just clarify that deposit to make sure it’s kosher, and never from an ineligible supply.

Let’s say that cash got here from one in all your different accounts, and also you merely transferred the cash between accounts.

You would offer an LOE to the underwriter explaining this. However that wouldn’t be the top of the story. In case your LOE included particulars of one other checking account, they’d absolutely need statements for that checking account as nicely to assessment the exercise to ensure every little thing provides up.

Typically, when you’re fortunate, you would possibly even be requested to provide you with one other letter of rationalization as a result of contents in your earlier LOE. In impact, an LOE for an LOE.

As you’ll be able to see, issues can get actually murky in hurry, so it’s greatest to maintain issues actually tidy earlier than making use of for a mortgage mortgage.

Not often are mortgage underwriters fully happy with every little thing that’s introduced to them. And the extra you place within the entrance of them, the extra possibilities they need to ask for, nicely, extra.

[Who are all the people involved in the mortgage loan process?]

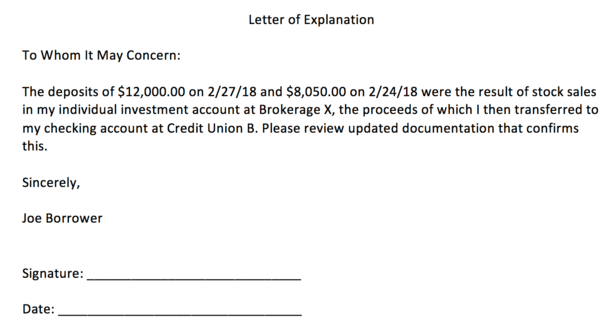

Letter of Rationalization Mortgage Template

- Embrace a fundamental heading and salutation to make it official

- A brief rationalization to resolve the confusion (brief and candy!)

- Signal and date it

- And supply essential documentation to backup the letter if wanted

- Try the pattern letter of rationalization beneath

You is perhaps questioning the best way to write a letter of rationalization (assuming one was requested of you).

The screenshot above is a pattern LOE template I created in a matter of minutes in case you’re questioning.

The excellent news is it’s tremendous straightforward to create one. It’s mainly only a Phrase doc (or comparable program) with a bit heading after which a quick paragraph or two to supply readability, adopted by your signature and the date it was written.

There aren’t any set formatting tips for an LOE, so you’ll be able to put the date on the high or the underside, and miss the salutation if you need. It doesn’t actually matter an excessive amount of so long as the important thing particulars are there.

You may put “Letter of Rationalization” or “Rationalization Letter” on the very high, adopted by a quick description of the problem at hand, then your title/signature/date. It actually doesn’t take a lot effort to create one.

That’s the simple half. The onerous half is perhaps offering supporting documentation, or making your case if don’t have a available rationalization.

What you write in these couple paragraphs is essential, so don’t rush the core message you’re making an attempt to convey.

Briefly, no matter you’re explaining has to make sense, and extra importantly, put the underwriter relaxed. They should really feel snug approving your mortgage, and no matter known as for the LOE to start with made them apprehensive.

It’s actually not the top of the world, and sometimes simply listening to in your individual phrases that X occurred due to Y is nice sufficient, with that supporting documentation to show it. Taking your phrase for it isn’t typically acceptable.

Both approach, don’t be afraid to ask the loan officer or mortgage broker precisely what they’re wanting to listen to, or how it’s best to format the letter. You probably have questions or are unsure, ask earlier than you submit paperwork that would get you in much more hassle.

Hold It Easy to Keep away from LOEs within the First Place

- Take into consideration what would possibly journey up the underwriter beforehand

- Take motion to resolve these issues earlier than you apply for a mortgage

- So an LOE isn’t essential to start with

- It will probably make life so much simpler and enhance mortgage approval possibilities

Your greatest transfer is perhaps to get all of your geese in a row lengthy earlier than making use of for a mortgage.

For instance, if it is advisable transfer some cash round, it could possibly be prudent to make these transfers 60+ days previous to the mortgage software.

Mortgage lenders sometimes solely ask on your last two monthly bank statements, so exercise that occurred prior shouldn’t be seen.

Any monetary exercise that takes place within the couple months previous to software may simply complicate issues, and require extra paperwork. And with that, scrutiny.

In case your accounts are comparatively untouched and nothing uncommon is current, ideally you’ll be able to skate proper via with out extra circumstances.

Similar goes for opening new accounts – when you don’t need to, don’t do it. It simply makes life extra sophisticated.

Should you’re enthusiastic about altering jobs, possibly wait. Something you suppose would possibly sound fishy or sophisticated is perhaps greatest to keep away from, for now. Or at the very least till that mortgage funds!

On the finish of the day, LOEs aren’t actually that tough to furnish or full, however they’ll result in larger issues when you don’t have good solutions!

As famous, do your greatest to play ball and make good with everybody, whether or not it’s the mortgage officer, processor, or underwriter, to keep away from pointless drama.

Lastly, if you’re requested to supply a letter of rationalization and aren’t positive why, communicate to your mortgage dealer or mortgage officer straight.

I typically get emails and feedback about why one is being requested. As an alternative of asking me, it’s most likely a greater concept to ask your dealer or consultant of the financial institution to unravel it as shortly as potential.

Learn on: What Do Mortgage Loan Processors Do?

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 18 years in the past to assist potential (and present) dwelling patrons higher navigate the house mortgage course of. Observe me on Twitter for warm takes.

[ad_2]

Source link