{kind=link}

Preparing article title...

[ad_1]

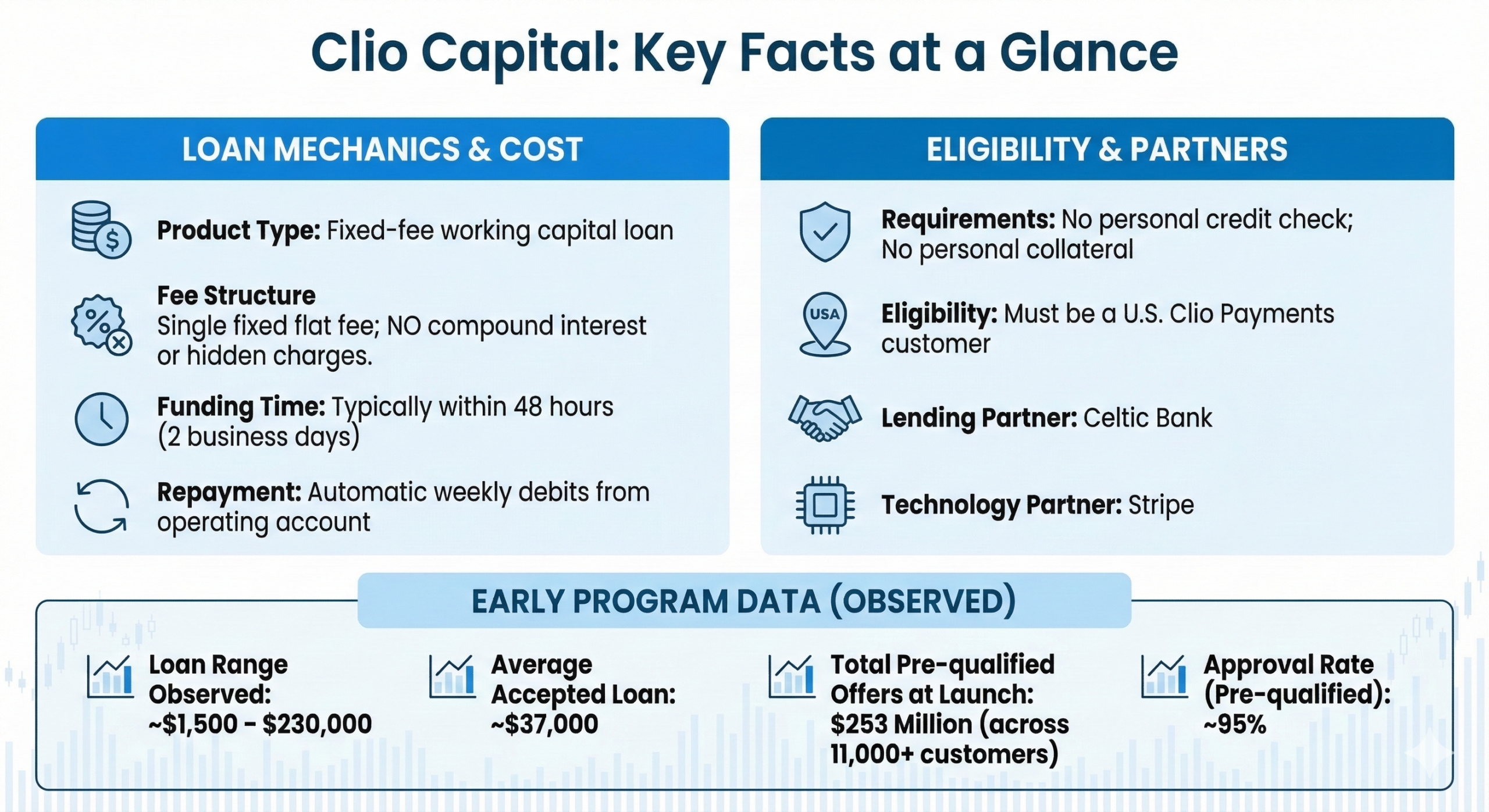

Clio has formally launched Clio Capital, a financing program designed solely for regulation corporations that use the corporate’s observe administration platform.

The product, which went stay Feb. 26, offers eligible regulation corporations with pre-qualified entry to working capital by means of a streamlined software course of straight throughout the Clio platform, bypassing the paperwork-heavy, rejection-prone course of that has traditionally made borrowing troublesome for small authorized practices.

In an interview with LawSites, A.J. Axelrod, Clio’s vice chairman of funds and monetary companies, stated this system had disbursed effectively over $1 million in loans inside its first week of full operation, with greater than 35 loans issued starting from $1,500 on the low finish to roughly $218,000–$230,000 on the excessive finish. Whereas nonetheless in its early days, this system’s common accepted mortgage quantity to this point is roughly $37,000.

In complete, as of launch, roughly $253 million in pre-qualified presents had been prolonged throughout greater than 11,000 Clio clients — although not all of these clients are anticipated to simply accept.

Clio Capital loans are issued by Celtic Financial institution and powered by Stripe. This system is offered now to eligible Clio Funds clients in the USA.

A Market Underserved by Conventional Lenders

Axelrod stated the motivation for Clio Capital was the structural market failure that has affected small companies — together with small regulation corporations — for many years. The normal mortgage course of is time-consuming, guide and infrequently discouraging, requiring candidates to collect monetary paperwork, go to a financial institution, full intensive purposes, and often face rejection even in spite of everything that.

Past the friction, Axelrod stated, banks typically have little financial incentive to lend small quantities. In consequence, corporations that want $1,500 or $5,000 could also be completely shut out of the normal lending market — and will as a substitute resort to carrying revolving bank card balances at rates of interest of 20–24% or increased.

Regulation corporations additionally face a problem particular to their {industry}. They usually lack the tangible property — gear, stock, actual property — that conventional lenders use as collateral. Current regulatory modifications to SBA lending guidelines have intensified these pressures, typically forcing companions to pledge private property akin to their houses to safe enterprise funding.

The time burden additionally falls disproportionately on attorneys. Each hour spent packaging financials for a financial institution mortgage is an hour not spent serving purchasers and producing income. For a lot of small agency homeowners, the calculus merely doesn’t favor pursuing a standard mortgage.

Pre-Qualification Based mostly on Funds Knowledge

What is especially attention-grabbing about Clio Capital is that it makes use of information that Clio already has about its clients to underwrite loans prospectively somewhat than reactively.

As a result of Clio, by means of its Clio Funds produce, processes funds for tens of 1000’s of regulation corporations, it has real-time visibility into billing frequency, fee volumes and associated monetary exercise. Clio Capital makes use of that information for a pre-qualification course of that evaluates all eligible Clio Funds clients on a rolling foundation.

Companies that meet eligibility standards obtain a pre-qualified supply straight inside Clio Handle, the corporate’s observe administration software. The supply features a mortgage quantity and rate of interest, and corporations can use a slider to regulate the quantity they wish to borrow.

As a result of clients are pre-qualified earlier than they provoke an software, Clio initiatives an roughly 95% approval price — that means solely about 1 in 20 clients who click on by means of to simply accept a suggestion will likely be declined.

A secondary layer of underwriting dietary supplements the funds information, Axelrod stated. Potential debtors are requested to attach their checking account (with their consent) in order that further alerts could be reviewed, akin to whether or not the agency has an energetic chapter or a sample of returned funds.

Axelrod described this step as designed to be as frictionless as potential, and stated it accounts for a lot of the instances through which pre-qualified clients are finally not permitted.

Finishing the appliance usually takes just a few minutes. The applying then enters a quick assessment queue — normally resolved inside a day — after which funds are transferred by way of ACH. Clio says most debtors obtain funds of their financial institution accounts inside roughly 48 hours.

That pre-qualification course of implies that eligibility relies on a agency’s enterprise efficiency throughout the Clio ecosystem — not on the private credit score scores of the agency’s companions. Debtors don’t must pledge private property as collateral.

Mortgage Construction and Pricing

Clio Capital loans are structured as conventional installment loans, that means they’ve a set compensation schedule with an outlined time period and a set complete value. There isn’t any compound curiosity, and Clio says there are not any origination charges, information processing charges or different add-on costs.

Axelrod stated the efficient rate of interest Clio has been seeing runs round 15%, which he described as meaningfully higher than typical bank card charges (roughly 22–24%) and aggressive with what a borrower would possibly count on from a top quality small-business mortgage.

He famous that some various lenders cost charges of 30–40% or obscure their true value with charges, neither of which applies to Clio Capital.

Every borrower’s supply is personalized based mostly on their particular person fee historical past and threat profile, so charges and out there mortgage quantities will fluctuate.

Compensation is dealt with by means of automated weekly debits from the borrower’s checking account, which Clio describes as designed to maintain money movement predictable with out requiring guide administration.

If debtors run into problem making repayments, Axelrod stated, Clio intends to work with them, doubtlessly by means of fee reduction or program modifications, somewhat than leaving them on their very own to navigate the scenario.

Partnering with Celtic Financial institution and Stripe

Clio isn’t itself a lender, financial institution or licensed depository establishment, and it doesn’t maintain the loans on its stability sheet. As a substitute, this system operates by means of a partnership construction that Axelrod described as drawing on the respective strengths of every participant.

Clio contributes what Axelrod characterised as its two most respected property for a lending program: distribution (direct entry to a big, engaged base of regulation agency clients) and information (detailed, real-time fee and billing data that can be utilized to underwrite credit score selections).

Celtic Financial institution, a Utah-chartered industrial financial institution, offers the regulatory standing and price of capital required to difficulty loans at aggressive charges. Stripe serves because the funds infrastructure underpinning this system.

Axelrod famous that navigating the regulatory panorama for lending — which includes each federal guidelines and state-by-state licensing necessities — is a big endeavor that Clio couldn’t effectively handle by itself.

The financial institution partnership permits Clio to supply a compliant product with out having to construct that regulatory infrastructure internally.

Privateness and Knowledge Use

Addressing potential privateness issues, Axelrod stated that Clio discloses all through the appliance course of precisely how buyer information can and can’t be used.

This system operates underneath what he described as an information wrapper, that means that the funds information and lending/compensation data collected as a part of this system can solely be used for functions inside that program and can’t be repurposed elsewhere inside Clio’s platform or operations.

For instance, if a borrower misses funds on a Clio Capital mortgage, Clio can’t use that data to have an effect on the shopper’s standing with respect to different Clio merchandise.

Axelrod stated Clio takes compliance throughout all dimensions of this system, not simply privateness, “extremely critically,” and he stated that the corporate selected best-in-class companions partially due to their compliance capabilities.

Who Is Eligible

At the moment, eligibility for Clio Capital requires {that a} regulation agency be an energetic Clio Funds buyer. Cost processing information is what drives the pre-qualification engine, so corporations that don’t use Clio Funds don’t but qualify.

Axelrod stated Clio hopes to broaden eligibility sooner or later by incorporating further information sources, in order that corporations utilizing Clio for observe administration however not funds would possibly finally qualify.

He famous that this system is beginning with funds information as a result of that information offers a high-confidence, real-time sign about enterprise well being that allows favorable underwriting phrases.

This system is at present out there solely in the USA. Axelrod stated the corporate intends to discover worldwide enlargement, however emphasised that regulatory complexity makes it vital to not rush into markets with out the correct companions in place.

How Companies Can Use the Funds

Clio doesn’t prohibit how debtors use their mortgage proceeds. The applying doesn’t require corporations to state a particular use of funds, and a agency’s acknowledged objective doesn’t have an effect on whether or not it’s permitted.

The early alerts counsel a broad vary of makes use of, Axelrod stated. Money movement administration is a typical motivation — small corporations with irregular income nonetheless face predictable obligations akin to payroll, lease and working bills.

Past that, corporations are utilizing capital to put money into development: new know-how, advertising, hiring and different initiatives that require upfront spending.

Axelrod additionally foresees that information on what forms of corporations apply for loans and the way they use them might finally yield significant industry-level insights.

Axelrod additionally foresees a potential optimistic suggestions loop in this system’s design. He expects that debtors who efficiently repay a mortgage will likely be shortly re-approved for brand spanking new financing — and doubtlessly eligible for bigger quantities at decrease charges. Profitable compensation is a powerful credit score sign, and Clio intends to make use of it to supply progressively higher phrases to dependable debtors.

The aim, as he described it, is to create a cycle through which corporations that achieve entry to capital, deploy it successfully, develop their observe, and repay their loans are progressively rewarded with cheaper, extra accessible financing.

Broader Fintech Enlargement

Clio Capital isn’t the corporate’s first foray into monetary companies. The corporate already presents Clio Funds, a fee processing product, in addition to a buy-now, pay-later function for authorized companies. Axelrod stated that Clio Capital represents an enlargement of that broader fintech technique, and that further monetary merchandise are into account.

He famous that completely different corporations have completely different financing wants. A revolving line of credit score, a multi-draw facility, or a service provider money advance would possibly serve some clients higher than an installment mortgage. Clio intends to hearken to buyer alerts and develop merchandise accordingly. The present installment mortgage was chosen as a place to begin as a result of it’s easy, clear and broadly relevant.

[ad_2]

Source link