{kind=link}

There’s been a variety of worry recently that mortgage rates could rise back above 7% or even higher this yr.

The motive force being inflation associated to $100+ oil, which will increase the price of nearly every thing.

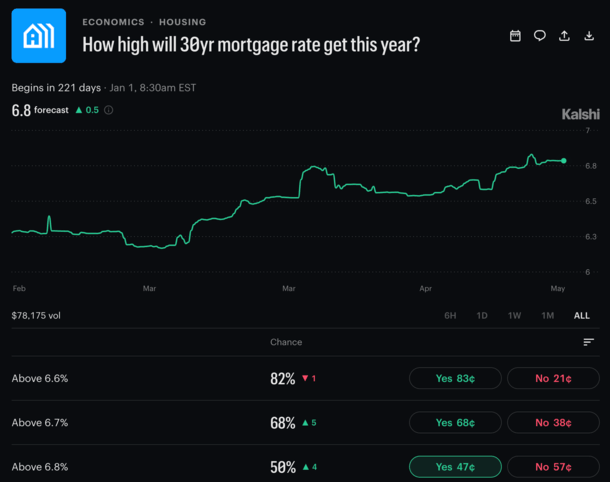

However the so-called “odds” are nonetheless fairly cut up with solely a 50% probability they rise above 6.8%, this in response to Kashi, which presents and tracks prediction markets.

This doesn’t imply they’re proper, however it exhibits you the place pricing is resolving in the meanwhile.

So maybe there’s restricted upside (in a foul means!) for the 30-year mounted, regardless of all that’s occurring.

Will the 30-Yr Mounted Rise Above 6.80% Once more This Yr?

Eventually look, Kalshi’s “How excessive will 30yr mortgage price get this yr” market is at a good 50-50 probability for rising above 6.8%.

That is at any level over the subsequent six months and alter which might be left within the yr 2026.

That’s not a lot conviction given everybody has been screaming that mortgage rates may surge increased with inflation.

It makes use of Freddie Mac’s weekly Main Mortgage Market Survey (PMMS) because the supply.

As of final week, the 30-year fixed averaged 6.51%, per the PMMS, so it must transfer about 30 foundation factors increased to get above that 6.8%.

Kalshi at present sells a “sure” contract for this marketplace for $0.47 every. So $100 price at $0.47 would purchase you 213 contracts.

The way in which it really works is if you happen to have been to stake $100 on the 30-year mounted going above 6.8%, and it hits, you’d earn $113 in revenue.

In different phrases, these contracts turn into price a greenback every if the 30-year mounted goes above 6.8%.

I’m not saying to do it, nor am I doing it, however I assumed it was an attention-grabbing means of possibilities based mostly on public notion.

The 30-Yr Mounted Was Above 6.8% in 16 of 52 Weeks Final Yr

I truly regarded again on mortgage charges in 2025 based mostly on Freddie Mac information and located that there have been 16 weeks the place the 30-year mounted was above 6.8% final yr.

That’s greater than 1 / 4 of the time, practically a 3rd in truth, when situations have been arguably comparatively comparable.

And thoughts you, we didn’t have the Iranian battle and oil costs above $100, with renewed fears of inflation.

That’s to not say mortgage charges return there, however it additionally wouldn’t shock me.

I’ve been saying for some time that charges may briefly contact 7% and even rise above 7% this yr.

In fact, it depends upon how Freddie Mac captures information.

Their weekly survey is usually delayed as a result of they acquire mortgage price quotes all through the week (prior Thursday through Wednesday) and submit them on Thursday.

This implies they usually don’t seize all the speed motion, particularly if it’s transient.

For instance, you may get a day or two when charges spike, however then they ease once more and Freddie Mac by no means actually captures it. Or it’s diluted by decrease days.

Conversely, you’d see that price motion on a day by day mortgage index akin to Mortgage Information Each day’s.

When it comes to when the 30-year mounted was final above 6.8%, it was the week of June 18th, 2025.

The massive distinction this yr versus final although is that mortgage rate spreads have improved tremendously.

This implies you want the 10-year bond yield to go even increased this yr, all else equal.

It’s actually nonetheless an actual chance, however it is going to be pushed by what transpires in Iran.

If a peace deal or comparable decision is reached anytime quickly, we would by no means get about 6.8%.

If the battle drags on or worsens, one thing above 6.8% and even 7% is fully conceivable.

The type of excellent news right here is that mortgage charges might need a little bit of a ceiling at present ranges, so the worst may principally be behind us.

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) dwelling patrons higher navigate the house mortgage course of. Observe me on X for warm takes.