{kind=link}

I used to be ICE’s most up-to-date Mortgage Monitor Report when one thing struck me.

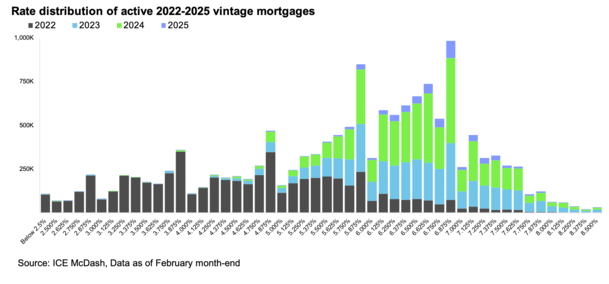

Of their price distribution chart of latest mortgages, I seen an excellent wide selection of charges in the course of the 12 months 2022.

This was as a result of the 30-year fastened started the 12 months round 3%, and ascended quickly to round 7.5% by that October.

It needs to be the worst 12 months on file for mortgage charges going way back to information go.

However one thing else popped out at me as properly, which could possibly be vital should you’re looking for a house mortgage.

2022 Grew to become a Horrible Yr for Mortgage Charges

As famous, 2022 was the worst 12 months for mortgage charges on file when it comes to motion.

Whereas the speed itself was decrease, solely rising above 7%, the magnitude of change is unmatched. Almost a tripling in charges.

That’s nowhere near the 18% mortgage rates in the 1980s, however the velocity and depth of change is second to none.

In 1981 the 30-year fastened started the 12 months at round 14.9%, per Freddie Mac. It then climbed to 18.45% that October earlier than rapidly calming down once more.

By 1982 it was again to the 13% vary, the place it stayed till 1985 as charges started their lengthy descent to the single-digits.

So whereas a price of seven.5% wasn’t notable, the rise in proportion phrases was fairly bonkers. Going from 3% to 7.5% is a 150% change.

Conversely, going from 15% to 18% is only a 20% change. Certain, large numbers, however a lot smaller adjustments percentage-wise.

Anyway, that was the primary cause I used to be learning this chart, pictured above. However not the explanation I’m scripting this put up.

The Vary in Charges Through the Yr Prolonged From the Mid-2s to the Excessive-7s

What was much more loopy about 2022 was the vary in charges supplied to debtors, as seen within the chart from ICE.

Some very fortunate debtors had been capable of snag sub-2.5% mortgage charges as late as 2022. So regardless of it being a horrible 12 months ultimately, many nonetheless made out very well.

In fact, they needed to get these mortgages closed within the first few months of the 12 months.

Principally by March charges had been within the 4% vary, and by April the 5% vary. And by June, you guessed it, the 6% vary.

The window was tight, however many nonetheless managed to get charges that began with a 2, 3, 4, and even a 5, which sounds not half-bad as we speak.

It really was a 12 months like no different when it got here to mortgage charges.

The truth that two debtors may sit down and ask what price they obtained, and one may say 2.5% and the opposite 7.5% tells you all the things you could know.

Be Cautious Which Mortgage Price You Select

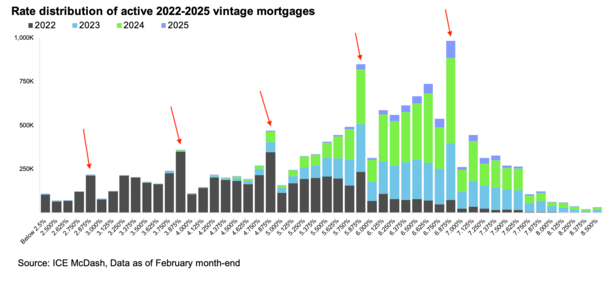

However right here’s what’s most attention-grabbing in regards to the chart. As I annotated above, take a look at the charges which have essentially the most energetic mortgages throughout all of the vintages (2022 to 2025).

It’s not the three% price, the 4% price, or the 5% price.

It’s the two.875% price, the three.875% price, the 4.875% price, the 5.875% price and the 6.875% price.

And why do you assume that’s? Why is that this seemingly random .875% price appended to essentially the most mortgages?

Properly, mortgage rates are offered in eighths, so the ultimate eighth accessible earlier than you hit the dreaded subsequent large quantity ends with .875%.

In different phrases, a borrower is extra more likely to be bought a price of 6.875% quite than 7% as a result of it simply sounds (and appears) so much higher.

What would you quite have? A price that begins with 6 or 7?

If you happen to take a look at the chart, you may see that charges ending in .875% had been the most typical in all of the vintages included.

For instance, in 2024 most debtors opted for a price of 5.875% as a substitute of 6%, or 6.875% as a substitute of seven.

In 2023, it was the identical two charges that had been hottest amongst householders.

In 2022, they opted for 3.875% and 4.875% essentially the most. And a few acquired 2.875%.

Whereas charges could have modified over time, the .875% nonetheless reigned supreme.

How A lot Are You Really Financial savings If Something at All?

Factor is, these sub-7% charges, or sub-6% charges is probably not a fantastic deal.

Let’s contemplate a $400,000 mortgage quantity at 6.875% versus 7%. The distinction in month-to-month cost is simply $34.

Now think about should you paid an additional $1,000 in closing prices to acquire that price.

You in contrast lenders however didn’t listen a lot to the closing prices. Properly, that $34 in financial savings will take about 30 months to recoup.

What occurs should you promote the house or refinance the mortgage earlier than then? You’d depart cash on the desk.

You wouldn’t understand the financial savings of the decrease price and it’d be merely a psychological victory having a price that began with a primary digit decrease.

The purpose I’m making an attempt to make right here is that choosing a price just under a key threshold (entire quantity like 6%, 7%, and many others.) may not be in your greatest curiosity, actually.

So when shopping mortgage rates, take the time to find out what mixture of price and shutting prices makes essentially the most sense primarily based on how lengthy you propose to maintain the mortgage/property.

Generally it’s actually better to take the higher mortgage rate.

And don’t get lured by one lender, who could cost you extra, merely to get a price that seems so much decrease than it really is. Be aware of the distinction within the month-to-month cost!

FYI, the identical precept applies to charges that finish in .99%, no completely different than once you purchase meals on the grocery retailer. However the distinction is even smaller!

Learn on: Watch Out for Low Mortgage Rates You Have to Pay For

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence patrons higher navigate the house mortgage course of. Comply with me on X for warm takes.