{kind=link}

These days, a number of mortgage charge quotes have required factors to be paid.

Referred to as low cost factors, they’re a form of prepaid interest due at closing that decrease your mortgage charge for all the mortgage time period.

For instance, you may be capable to get a charge of 5.99% when you pay one level as a substitute of paying nothing and settling for a charge of say 6.25%.

The tradeoff is when you preserve the mortgage lengthy sufficient, you win through decrease month-to-month funds (and fewer curiosity paid).

But when rates of interest all of the sudden drop, you is likely to be enticed to refinance to avoid wasting much more, thereby giving up your previous paid for charge.

What’s the Mortgage Fee Outlook?

Whereas mortgage charges have been on a relative tear the previous 15 months and alter, they continue to be elevated.

In spite of everything, many huge banks and lenders are nonetheless quoting charges for a 30-year mounted within the 6s.

That compares to charges within the 2s, 3s, and 4s again in 2022. In fact, these had been totally different days and fueled by the Fed’s QE program the place they purchased trillions in MBS.

Some folks assume they’ll do it once more, however many others assume it’s a protracted shot.

It’s no secret the Trump administration needs to decrease housing prices, and Trump campaigned on bringing mortgage rates back to 3%, or even lower!

However a number of issues are promised throughout campaigning which are in the end by no means delivered.

So banking on that might be akin to a lottery ticket. It might occur, however most likely gained’t.

As an alternative, your finest guess is to take a look at the underlying financial information to find out the near- and long-term mortgage rate outlook.

As said, we’ve made a number of progress on charges, which regardless of being at file lows in early 2022, rose to eight% in late 2023, and are actually usually quoted within the 5s.

That’s not too shabby, however you do marvel if they will get even higher because the 12 months goes on.

In case you imagine they will and also you’re in want of a mortgage at present, you may assume to your self, pay nothing at closing and preserve your eyes on a refinance down the road.

For instance, if you may get a 6% charge at present with no factors and restricted or no charges, you possibly can keep away from a number of out-of-pocket prices and depart nothing on the desk if charges drop.

If mortgage charges drift decrease later this 12 months, unexpectedly you possibly can apply for a rate and term refinance and snag one thing within the lower-5s.

Presumably with out a lot in the best way of closing prices in addition!

Lengthy story brief, it’s important to decide how lengthy you anticipate to carry your mortgage (and the property when you’re at it).

It’s simpler mentioned than accomplished clearly, and timing something is usually a idiot’s errand.

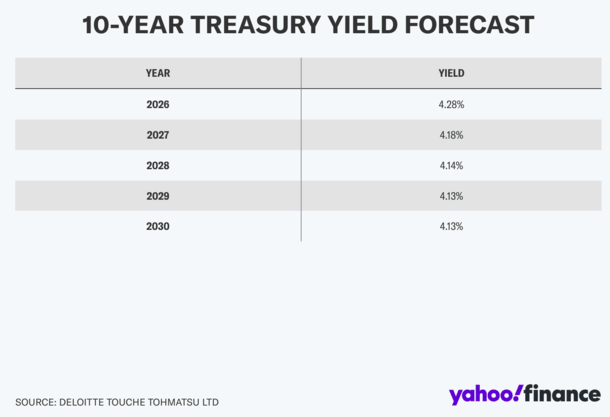

The ten-Yr Bond Yield May Be Flat By the Yr 2030

The explanation I convey all this up is as a result of there are forecasts on the market that anticipate little to no motion within the 10-year bond yield, which is a good bellwether for 30-year fixed mortgage rates.

Deloitte is at present forecasting a 10-year bond yield that’s primarily unchanged over the following 5 years.

If it barely strikes from now till the 12 months 2030, likelihood is mortgage charges may even be principally caught.

Sure, there’s the spread component of rates, which is the distinction between the 10-year bond yield and 30-year mounted charge.

Nevertheless it’s normalized fairly a bit already, and won’t be capable to are available rather more both.

So when you imagine all that, this could possibly be near pretty much as good because it will get for mortgage charges for a while.

Assuming that’s the case, you possibly can then make the argument to pay discount points at closing to buy down your rate.

Why? As a result of mortgage charges gained’t get any higher so that you’ll possible preserve your mortgage longer and a decrease purchased down charge can be extra helpful because of this.

Nonetheless, that is once more only one concept. Mortgage charges might in actual fact fall greater than predicted and begin with a ‘4’ sooner or later, then your paid factors could be a waste when you refinanced the speed away.

You May Experience It Out with an ARM As an alternative

One different to think about, assuming you assume mortgage charges gained’t go up, however might come down, could be an adjustable-rate mortgage.

You might take out a 5/6 ARM or a 7/6 ARM, each of which provide a set charge for a number of years earlier than the primary adjustment.

In addition they include an rate of interest low cost versus the 30-year mounted as a result of they finally turn into adjustable.

Then you possibly can regulate charges and in the event that they do come down, you possibly can refinance into a set mortgage if you would like that certainty (or a brand new, cheaper ARM…).

That might provide the better of each worlds, the decrease charge at present and the optionality to refinance if charges vastly enhance.

In the event that they don’t, your ARM wouldn’t be an excessive amount of of a threat, particularly if short-term charges come down greater than long-term charges.

The one caveat is you’d should qualify for a mortgage when you wanted to refinance sooner or later (if say charges spiked increased in your ARM). Which means having a stable job, revenue, and credit score to get authorized.

With a 30-year mounted, you wouldn’t completely must exit and get a brand new one, even when charges elevated (or dropped and also you needed to take benefit).

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and current) residence consumers higher navigate the house mortgage course of. Observe me on X for warm takes.