{kind=link}

Properly, there’s a silver lining to every part.

And whereas the U.S. financial system seems as if it’s faltering, at the least mortgage charges are decrease, proper?

It’s clearly bittersweet, however the one actual technique to to get higher mortgage charges with out direct intervention is with cool financial knowledge.

Decrease inflation would in all probability be probably the most very best means of reaching that, however tariffs have clouded that path.

As an alternative, it seems employment knowledge is doing the heavy lifting to deliver down mortgage charges, for higher or worse.

The Unwinding of Final 12 months’s Scorching Jobs Report

What’s sort of fascinating is we’re mainly simply unwinding the recent jobs report that arrived again on October 4th, 2024.

That now notorious September 2024 jobs report is what propelled mortgage charges larger, proper after the Fed pivoted after 11 consecutive price hikes.

Due to the awkward timing, many assumed it was the Fed cutting that pushed mortgage rates higher.

When actually it was the ultra-hot, sudden jobs report launched simply two weeks after that basically did the injury.

In case you recall, that blowout jobs report revealed that the U.S. financial system added a whopping 254,000 jobs final September.

That greater than exceeded expectations that referred to as for a mere 142,500 new jobs added.

On the identical time, each the July and August jobs stories for 2024 have been revised larger, by 55,000 and 17,000, respectively.

That’s what did it. It wasn’t that the Fed had some magical powers the place no matter they did, mortgage charges did the other.

For the file, the Fed doesn’t control mortgage rates whether or not they go up or down. It’s actually simply random and relies upon what else is occurring within the financial system.

Final yr, there was just a little little bit of a promote the information second when the Fed lastly reduce, however that was after 30-year fastened mortgage charges had fallen from 8% to almost 6% in lower than a yr.

So a transfer like that was anticipated. The necessity to blow off steam made sense.

Right here we’re once more in an identical boat. It’s virtually déjà vu.

Besides this time, it seems we’re unraveling that sizzling jobs report from a yr in the past. Sort of ironic.

Labor Has Gone Chilly, and Mortgage Charges Like That

- ADP mentioned personal sector employment elevated by simply 54,000 jobs in August

- That was under the consensus estimate of 75,000 jobs added

- The JOLTS report revealed job openings fell to the bottom level in practically a yr in July

- And a chilly August jobs report from the BLS tomorrow could possibly be the icing on the cake

In contrast to final yr, the pattern currently has been a cooling labor market.

As an alternative of a shock sizzling jobs report, a month in the past we got a surprise ice-cold jobs report for July.

And just like a yr in the past, we bought revisions, besides this time they have been downward revisions.

Primarily, the exact opposite of what transpired final yr.

That has been the driving force of decrease mortgage charges currently, similar to the recent jobs a yr in the past drove them larger.

The massive query now could be if it continues. It definitely seems as if it’s going to, although like mortgage charges on the whole, there are at all times surprises. And it’s exhausting to foretell what’s going to occur.

However I can let you know that the roles report being launched tomorrow is a really large second for mortgage charges.

It’s going to both reinforce this downward pattern we’ve been on, with 30-year fastened charges falling about 75 foundation factors (0.75%) from the beginning of the yr.

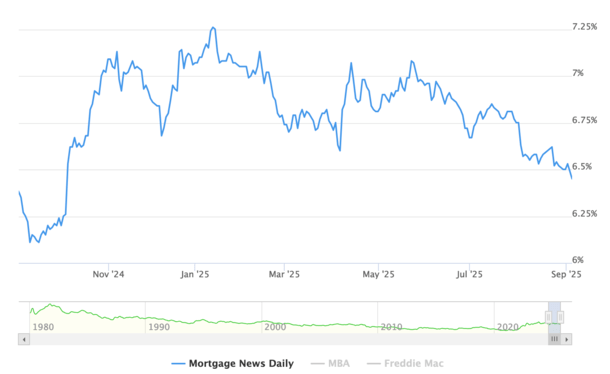

Per MND, mortgage charges have fallen from round 7.25% to start out the yr to six.45% at present.

Or it might show to be one more head faux, the place mortgage charges unexpectedly reverse course after exhibiting plenty of promise.

The dilemma we face now could be that in an effort to get even decrease mortgage charges, we want labor to proceed to indicate indicators of weak spot.

And clearly that’s not good for our financial system as a complete. So it’s tough to root for unhealthy information simply to get decrease mortgage charges.

Sadly, that’s sort of the place we’re at proper now. Maybe there’s a center of the street situation the place labor doesn’t considerably weaken, however doesn’t shock to the upside both.

Learn on: How are mortgage rates set?

Earlier than creating this web site, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence patrons higher navigate the house mortgage course of. Observe me on X for decent takes.