{kind=link}

It’s been a tough week for mortgage charges, that are reeling because of new aggressions within the Center East.

The ceasefire that started on June seventeenth is outwardly no extra, with main strikes exchanged between the U.S. and Iran over the previous couple days.

That’s placing renewed stress on oil costs, bond yields, and naturally mortgage charges.

However regardless of all that, the chances of the 30-year mounted rising considerably greater from right here stays fairly low.

That’s in the event you imagine the chances…

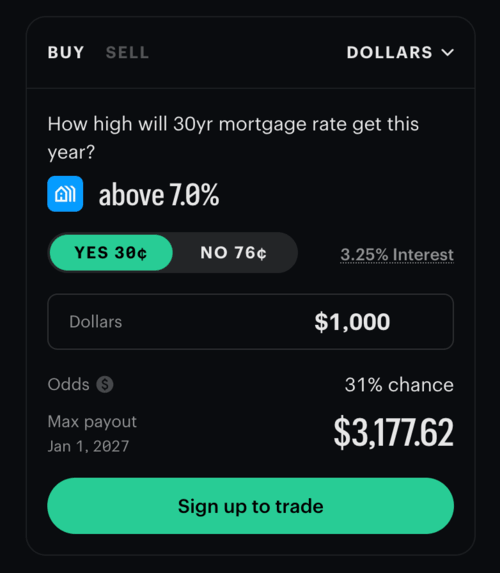

Solely a 28% Likelihood the 30-Yr Fastened Rises Above 7%?

The most recent odds from prediction market Kalshi reveal there’s solely a 28% “probability” that the 30-year mounted climbs above 7.0% in some unspecified time in the future this 12 months.

For reference, the 30-year mounted is at present averaging 6.43%, based mostly on Freddie Mac’s weekly mortgage charge survey.

That quantity is bound to climb once they launch their replace at this time, however it’s solely about 50 foundation factors away from being within the cash.

In the meantime, all I hear is individuals saying mortgage charges are going again to 10% or greater!

Or that they’ll be within the double-digits quickly sufficient. Blah blah blah.

Then I feel to myself, we will’t even break 7% and also you’re telling me they’re going to 10%?

Evidently the excessive rate of interest predictors are pushed extra by emotion than precise logic.

They need greater rates of interest as a result of they assume it’ll sort things and cease costs from going greater and better.

Maybe, however are such charges truly warranted? It’s not the Eighties over again.

Sure, we’ve got an power shock of kinds, however we’re additionally much more power unbiased at this time than again then.

The Fed additionally is aware of find out how to handle inflation rather a lot higher at this time versus that point because of errors discovered alongside the way in which.

So to assume rates of interest are going to rival these seen within the Eighties when the 30-year fixed briefly spiked to 18% could be a bit foolish.

And it may also clarify why even the chances to creep up even one other 50 bps stays an extended shot.

How Might Mortgage Charges Get Again to 7% or Increased?

Now simply because the chances are low doesn’t imply it may well’t occur.

There have been loads of situations the place the sudden has occurred and underdogs have cashed.

Kalshi makes use of Freddie Mac’s Main Mortgage Market Survey (PMMS) to find out the result and as famous, it’s at present round 6.50%.

To ensure that mortgage charges to climb one other 50 bps this 12 months, we’d want quite a lot of sustained sizzling financial knowledge to come back by way of.

The two key drivers of mortgage rates are inflation and labor data.

Which means we’d want sizzling CPI, PPI, and PCE prints together with sizzling jobs experiences for the following few months, maybe with no let up.

Final month, inflation rose above 4% for the first time in three years, per the Bureau of Labor Statistics (BLS), however it was principally tied to unstable power costs associated to the Iranian battle.

As soon as power and meals had been stripped out, core CPI was up simply 2.9% from a 12 months earlier.

Nonetheless elevated and above the Fed’s 2% goal and presumably sufficient to entertain some charge hikes later this 12 months if it doesn’t enhance.

Nevertheless, there’s additionally the labor market, and that hasn’t been so sizzling these days. The latest experiences weren’t ice chilly by any stretch, however the Fed nonetheless has to steadiness inflation and jobs.

And if jobs stay weak, they could be restricted in how a lot they’ll hike, that means one or two 25-bp hikes could possibly be it, regardless of inflation issues.

The takeaway right here is regardless of inflationary headwinds, a lot of it not too long ago tied to the struggle, the financial system doesn’t look so robust.

So even when there’s some upward stress on rates of interest, it may show to be short-lived and likewise offset by rising unemployment.

Lastly, let’s not overlook that mortgage charges are up almost 0.75% because the finish of February when the battle started, so quite a lot of danger is already baked in.

That’s why a 7% mortgage charge, which doesn’t even sound all that unlikely, may stay elusive.

Earlier than creating this website, I labored as an account govt for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 20 years in the past to assist potential (and present) house consumers higher navigate the house mortgage course of. Observe me on X for decent takes.