{kind=link}

I generally overlook your common house owner doesn’t know all of it with regards to mortgages.

They’re complicated and complicated and what might sound apparent to me isn’t to others.

Newest living proof was an e mail my good friend acquired from his mortgage servicer about tapping his fairness.

It listed his estimated residence worth and estimated “money obtainable” if he had been to take out a second mortgage, comparable to a house fairness mortgage or HELOC.

He was confused as a result of the numbers didn’t add up based mostly on what he owed.

Lenders No Longer Let You Borrow 100% of Your House’s Worth

The confusion may lie in how lenders’ threat appetites have modified through the years.

Again within the early 2000s, it was quite common for banks and lenders to let debtors take out loans at 100% LTV/CLTV, which means each final greenback was cashed out.

For instance, if your private home was appraised for $500,000 again when, a lender could have allow you to borrow all the $500,000!

Looking back, this clearly wasn’t a good suggestion for what looks like very apparent causes right now.

Zero pores and skin within the recreation, excessive borrowing prices, little motive to stay round if the going will get powerful and/or the property worth all of the sudden declines.

And that’s precisely what occurred. Making issues worse again then was the prevalence of adjustable-rate mortgages and even negative amortization loans and second mortgages up to 125%!

All of us now realize it was tremendous dangerous lending that hopefully by no means will get repeated. That scenario led to one of many biggest housing crashes in history.

It additionally led to new mortgage guidelines, together with the ATR/QM rule, which places numerous guardrails in place to stop one other main disaster.

With out getting too convoluted right here, let’s simply say lenders are much more cautious right now, fortunately.

What this implies is you’ll be able to not take out a mortgage for 100% of the property worth. Lenders desire a buffer.

Most Lenders Cap House Fairness to 80% or Much less These days

Due to the newest mortgage disaster, banks and lenders stay much more conservative.

They wish to make sure the loans they make aren’t too dangerous, and even when the borrower falls behind, they will recoup any losses.

One of the best ways to perform that is to require a buffer between what the borrower owes and what the property is price.

That means in the event that they must foreclose, there’s hopefully some fairness and the property received’t promote for lower than what it’s price.

It was widespread again then for debtors to have unfavourable fairness, also referred to as an underwater mortgage, due to the excessive most LTVs/CLTVs and the speedy residence worth declines.

At present, you’re typically going to be capped at say 80% CLTV when taking out a second mortgage like a HELOC or home equity loan.

This ensures there’s at the least 20% in fairness if issues go sideways. Or maybe residence costs drop!

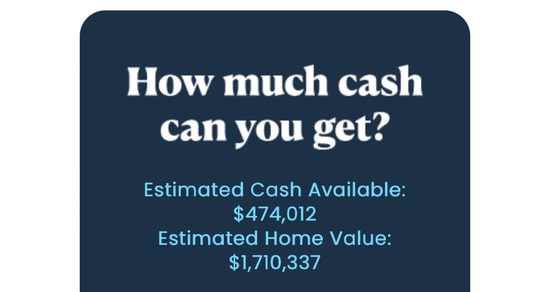

So when my buddy was doing the mathematics, he was confused as a result of he solely owes one thing like $800,000 and it stated his residence was price $1,700,000.

In his thoughts, that meant he may faucet one thing like $900,000, way more than the $474,000 talked about.

If we do the mathematics, this implies his specific lender is capping the max money out at 75% CLTV.

Roughly $1,275,000 divided by $1,710,000 is just below 75%. So on this case, a 25% fairness buffer.

That’s good for the lender as a result of it offers them a stable cushion. It’s additionally good for the well being of the housing market if residence costs fall and/or debtors fall behind on funds.

It helps us all keep away from one other situation the place householders get in over their heads and utterly sap their fairness, which might make a standard sale very troublesome.

Learn on: How to compare HELOCs from different lenders.

Earlier than creating this website, I labored as an account government for a wholesale mortgage lender in Los Angeles. My hands-on expertise within the early 2000s impressed me to start writing about mortgages 19 years in the past to assist potential (and present) residence consumers higher navigate the house mortgage course of. Observe me on X for warm takes.